TOPICS: ·automation impact·Basic Income

RELEVANCE: ·bad·not sure

Topic » Basic Income · [Clear All]

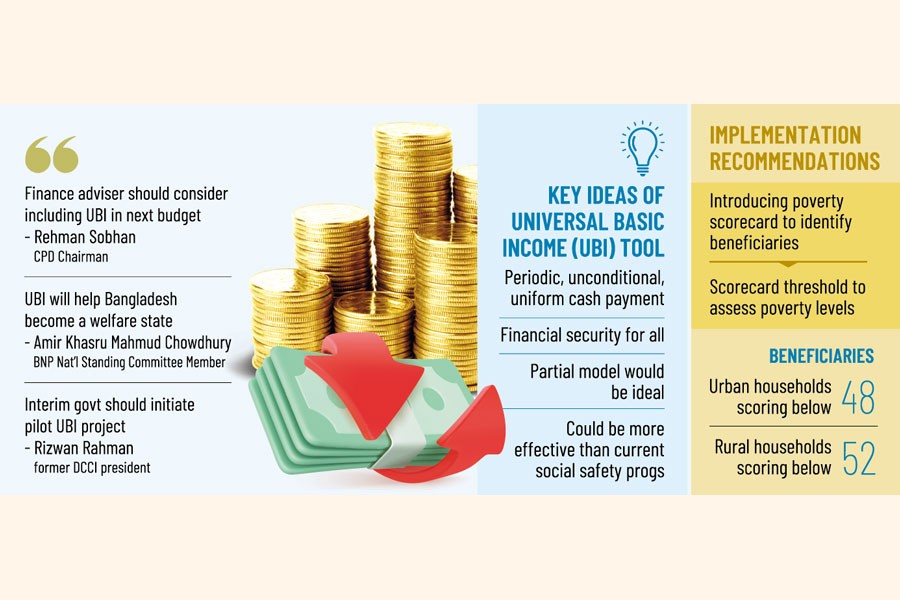

UBI promising poverty-reduction tool: CPD

November 24, 2024 · · Topic: Basic Income · Relevance: not sure November 24, 2024 · · Topic:

November 24, 2024 · · Topic:

The Centre for Policy Dialogue (CPD) has proposed universal basic income (UBI) for Bangladesh as a promising tool to reduce poverty, empower citizens, and streamline social protection even within the constraints of the current fiscal framework.

The local think tank made the proposal at a seminar titled "Assessing the Viability of Universal Basic Income in Bangladesh: Target Population, Fiscal Requirements, and Institutional Challenges" in a city hotel on Sunday.

The proposal said the UBI would include a periodic, unconditional, and uniform cash payment system, offering financial security to all members of society.Referring to several UBI schemes worldwide, the CPD said a […]

Full Post at today.thefinancialexpress.com.bd

Editorial: S. Korean gov’t must move beyond populist handout policies to address polarization

November 23, 2024 · · Topic: Basic Income · Relevance: not sure

President Yoon Suk-yeol delivers remarks at the 56th national prayer breakfast held at the Shilla Hotel in Seoul on Nov. 22, 2024. Yoon pledged to address polarization during the latter half of his term to ensure all citizens can contribute to national development. /Presidential Office As South Korean President Yoon Suk-yeol enters the second half of his term, he has set “addressing polarization” as a new policy priority, signaling a potential departure from the government’s traditionally conservative fiscal stance. Reports indicate that the administration is now weighing a more active fiscal approach, including the possibility of a supplementary budget, […]

Full Post at www.chosun.com

Guaranteed Income Supplement: 7 Facts Every Canadian Senior Must Know

November 23, 2024 · · Topic: Basic Income · Relevance: not sure

The Guaranteed Income Supplement (GIS) is a vital non-taxable financial aid provided by the Government of Canada. It is designed to support low-income seniors who rely on the Old Age Security (OAS) pension. Here are seven key details about this essential program: 1. Eligibility Requirements

You must be 65 years or older and reside in Canada.

You must already receive the OAS pension. Your annual income must fall below certain thresholds: Less than $22,056 for single, widowed, or divorced individuals. Less than $29,136 combined income if your spouse receives the full OAS pension. Additional thresholds apply for spouses […]

Full Post at www.soscip.org

Expectations of Liberation War unfulfilled: Rehman Sobhan

November 23, 2024 · · Topic: Basic Income · Relevance: bad

Image description Economist Rehman Sobhan on Saturday lamented that his expectation to see a discrimination-free society after the War of Independence in 1971 has not been fulfilled till date.

The social and economic disparities have grown, he said while addressing a discussion and launching of eight publications on marginalised communities in the capital.

Amid the trend, the problems of the marginalised communities have become acute, said Rehman Sobhan, also chairman of local think-tank Centre for Policy Dialogue.The celebrated economist, who will turn 90 in the next March and still loves romantic imaginations to solve the social and economic discriminations, said that […]

Full Post at www.newagebd.net

This state gives away $4,530 payments for Christmas: Here’s how to get yours

November 23, 2024 · · Topic: Basic Income · Relevance: not sure

This state gives away $4,530 payments for Christmas: Here’s how to get yours 1 Californians are in for a very merry Christmas after the announcement that the US Internal Revenue Service is distributing $4,530 Stimulus Payments before the end of 2024. The payments will be even higher for citizens with dependents. California is not the only state offering Stimulus Payments, and the aim of distributing these funds is to make up for shortfalls caused by inflation and the rising cost of living, and also offset some of the lasting adverse consequences of the COVID-19 pandemic on local economies. $4,530 […]

Full Post at www.eldiario24.com

CPP, OAS & GIS Pension Payment Coming on these Dates in December 2024 – Will you get this?

November 23, 2024 · · Topic: Basic Income · Relevance: bad

CPP, OAS & GIS Pension Payment Coming on these Dates in December 2024 : If you’re a senior in Canada relying on Canada Pension Plan (CPP) , Old Age Security (OAS) , or the Guaranteed Income Supplement (GIS) , understanding the payment schedule, eligibility criteria, and tips for maximizing your benefits is essential. The next payment date for all three programs is Friday, December 20, 2024 . CPP, OAS & GIS Pension Payment Coming on these Dates in December 2024 This guide covers everything you need to know to ensure you receive your payment on time and plan for […]

Full Post at lkouniexam.in

FD Rate: These 10 banks are giving up to 8% interest on 1 year FD, know the details

November 23, 2024 · · Topic: Basic Income · Relevance: not sure

FD Rate: These 10 banks are giving up to 8% interest on 1 year FD, know the details By investing in FD, customers get guaranteed income after a certain period. Currently, the country’s big private and government banks are giving excellent returns on FD.

If you are planning to invest in Fixed Deposit (FD) then this news is useful for you. Actually, by investing in FD, customers get guaranteed income after a certain period. Let us tell you that at present, the big private and government banks of the country are giving great returns on FD. Apart from this, […]

Full Post at www.informalnewz.com

Council Accepts Report on Efforts to Combat Rising Homelessness

November 23, 2024 · · Topic: Basic Income · Relevance: bad

Supports Letter to Port advocating environmental mitigation

On November 19, City Council accepted the 2024 Progress Report on The Road Home, A City’s Five-Year Strategic Plan to Prevent and Respond to Homelessness in Alameda . Health and Human Services Manager C’Mone Falls reported that despite the City nearly doubling its capacity to shelter and house its residents over the last three years, unsheltered homelessness is increasing and the need for investment remains.

Council supported a letter to the Port of Oakland Board of Commissioners reiterating environmental concerns about the Oakland Airport Terminal Modernization and Development Project and advocating for mitigation […]

Full Post at alamedapost.com

If we had universal basic income, would you still work?

November 23, 2024 · · Topic: Basic Income · Relevance: not surethevamp114 reblogged this from deermouth

mayo-spider liked this

thevamp114 liked this aldreantreuperi liked this princess-sheep reblogged this from gumi-megpoidd princess-sheep liked this notsurehowimfeelingaboutallthis reblogged this from musictherapy611 justen1d liked this aqua-aura reblogged this from soxry crabhaven reblogged this from yondamoegi lurker-at-thresholds liked this tinma liked this crabhaven liked this eritela liked this mattiebluebird liked this archangelbecca reblogged this from triaelf9 archangelbecca liked this aqua-aura liked this sexy-mothman reblogged this from pizzopaps papi-serpiente liked this obviousbaitfish reblogged this from gorps […]

Full Post at peachdoxie.tumblr.com

From Subsidized Housing to Homeownership: A Single Mom’s Journey of Growth, Grit and Guaranteed Income

November 22, 2024 · · Topic: Basic Income · Relevance: not sure

Front & Center is a groundbreaking Ms . series that began as first-person accounts of Black mothers living in Jackson, Miss., receiving a guaranteed income from Springboard to Opportunities’ Magnolia Mother’s Trust (MMT). Moving into the fourth year and next phase of this series , the aim is to expand our focus beyond a single policy intervention to include a broader examination of systemic issues impacting Black women experiencing poverty. This means diving deeper into the interconnected challenges they face—including navigating the existing safety net; healthcare, childcare and elder care; and the importance of mental, physical and spiritual well-being. […]

Full Post at msmagazine.com

Dreamers can now enroll in Covered California

November 22, 2024 · · Topic: Basic Income · Relevance: bad

Kim Johnson, Secretary of the California Health and Human Services Agency at the Covered California kickoff campaign in Los Angeles on Nov. 13, 2024. Photo by Zaydee Sanchez for CalMatters Good morning, Inequality Insights readers. I’m Wendy Fry.

California has expanded its health insurance marketplace, Covered California, to allow Deferred Action for Childhood Arrivals recipients to purchase subsidized health plans, CalMatters’ health reporter Ana B. Ibarra reports . This is a result of a federal rule that aims to provide health coverage to thousands of “Dreamers,” particularly those who are self-employed or lack other insurance options.

But the expansion coincides with […]

Full Post at calmatters.org

Multnomah County’s universal basic income experiment worked, until the money ran out

November 22, 2024 · · Topic: Basic Income · Relevance: not sure

Voycetta White was one of 100 Black mothers and caregivers participating in Multnomah County’s guaranteed income program focused on pulling people out of poverty. Sean Meagher/The Oregonian It was 7 a.m. on a warm August morning and Voycetta White had just finished an eight hour shift at the Best Western Vancouver, where she works as a night auditor. By 8 a.m., she would need to be at Legacy Good Samaritan Medical Center in Portland for another grueling eight hours of work as an optician — a trade she picked up while in prison .

Amid the hustle, White’s youngest daughter […]

Full Post at www.oregonlive.com

Help change lives! Volunteer with the Community Volunteer Income Tax Program

November 22, 2024 · · Topic: Basic Income · Relevance: not sure

November 22, 2024 – Canada Revenue Agency: The Community Volunteer Income Tax Program is an essential initiative of the Canada Revenue Agency that requires host organizations and volunteers to register or renew their registration each year.

As many government credit and benefit payments are income-tested, filing an annual income tax return is necessary, even for those with no income to report or whose income is tax-exempt.

For those who face barriers to doing their taxes, the Community Volunteer Income Tax Program (CVITP) can help.Through this free program, community organizations and their volunteers assist vulnerable persons to file their taxes and access […]

Full Post at employmentjourney.com

Universal Basic Income or Employment? A Debate About the Future of Work [44:26]

November 22, 2024 · · Topic: Basic Income · Relevance: not sure30 Minutes Plus

Sort by:

Best AutoModerator • 3h ago • r/mealtimevideos is your reddit destination for medium to long videos you can pop on and kick back for a while. For an alternate experience leading to the same kind of content, we welcome you to join our official Discord server . I am a bot, and this action was performed automatically. Please contact the moderators of this subreddit if you have any questions or concerns. Top 1% Rank by size Public r/mealtimevideos Kevin McCloud visits the Dharavi slum in Mumbai, reflecting on the lessons Western cities could learn from […]

Full Post at www.reddit.com

Campaign trail: With one week to go, parties are putting it all on the table

November 22, 2024 · · Topic: Basic Income · Relevance: not sure

Taoiseach Simon Harris gokarting with Cllr. Linda Nelson Murray in The Zone Mullaghboy, Navan, Co. Meath on Thursday night Fergal Phillips/Fine Gael

day 15

Here’s what’s happening on the campaign trails today. 2.0k 22IT’S DAY 15 and there’s only one week to go until voters take to the polling stations. Here’s what’s happening today: People Before Profit TD Gino Kenny will be in the Dublin mid-west constituency, where he’ll be speaking about the party’s election manifesto proposals to decriminalise drugs and make cannabis legal. MEP Luke Ming Flanagan will be joining him. Meanwhile, People Before Profit’s environment spokesperson Paul Murphy […]

Full Post at www.thejournal.ie

The harm of guaranteed basic income

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Unconditional cash did nothing to raise recipients out of poverty; Madison and Milwaukee have dabbled with idea

Results from the nation’s most comprehensive experiment in offering people a guaranteed basic income offer a warning to those places — including some Wisconsin cities — dabbling with the idea: Unconditional cash payments did nothing to permanently lift participants out of poverty and dependency. A three-year study of 3,000 people in Illinois and Texas found that those paid a guaranteed income atop any other public benefits worked less, were less likely to work at all, and their households’ income fell relative […]

Full Post at www.badgerinstitute.org

This chart shows how crazy fast the value of Elon Musk’s xAI has risen in 16 months

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Elon Musk’s AI startup launched in July 2023. It’s now valued at a reported $50 billion.The Washington Post/Getty, Tyler Le/BI Elon Musk’s AI startup xAI has been valued at a reported $50 billion, 16 months after its founding.

It hit the milestone nearly nine years faster than it took rival OpenAI to cross the threshold.

The funding round widens the valuation gap between xAI and its rivals like Anthropic and Perplexity. ADVERTISEMENT Recommended articles news Some community college kids in LA will now get a $1,000 monthly basic income news Google’s search business is all about distribution. The […]

Full Post at africa.businessinsider.com

Basic Income Grant coalition in Namibia protests conditional basic income grant

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Basic Income Grant coalition in Namibia protests conditional basic income grant

Basic Income Grant coalition in Namibia protests conditional basic income grant By Veripuami Kangumine

See original post here. The Basic Income Grant (BIG) Coalition of Namibia protested against the government’s proposed basic income grant on Saturday. They say the grant excludes the majority of the population. This comes after the Ministry of Gender Equality, Child Welfare and Poverty Eradication began registering qualifying households countrywide for the conditional BIG of N$600 last week.BIG Coalition coordinator Rinaani Musutua says the government has not made an effort to collaborate with the […]

Full Post at basicincometoday.com

Workers at Canada Post Are On Strike. Here’s What Postal Workers Are Fighting For.

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Explainer

Postal workers say they are fighting to protect pensions, improve working conditions and push for higher wages that keep pace with inflation

November 21, 2024Wondering why you haven’t received that package you were waiting for?Postal workers across the country are currently striking for better wages, protection of their pensions and to address health and safety concerns on the job.55,000 members of the Canadian Union of Postal Workers have been on a massive nationwide strike since Friday after negotiations at the bargaining table stalled with their employer Canada Post.Here’s why postal workers are pushing back against Canada Post’s “race to […]

Full Post at pressprogress.ca

CPP Payment Increase 2025 – What are the Expected Changes in Canada Pension Plan for Next Year?

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

The Canada Pension Plan (CPP), which offers financial assistance to employees throughout their retirement years as well as to the families of those who become handicapped or die, is an essential component of Canada’s social security system. As per rumors, CPP Payment Increase 2025 has been announced by the Canadian government as 2025 draws near, and it may have an impact on when and how much you get.

Millions of Canadians will be directly impacted by these changes in their retirement planning, particularly those who are getting close to retirement age. Monthly payments for retirees will climb by up to […]

Full Post at bsebmatric.org

Become an Uber Driver: Earn Guaranteed Income of $1444 for 146 Trips

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

1504076092-2

Date Posted:

Recruiter: Uber Location: California, Missouri Salary: On Application Job Description Drive with Uber and earn a guaranteed minimum of $1444 when you complete 146 trips in your first 30 days! Why Choose Uber? Driving with Uber offers an excellent opportunity to enhance your income while enjoying the flexibility to fit your lifestyle, whether you are looking for a gig, part-time, full-time, seasonal, hourly, or temporary work. Key Highlights: Quick Signup: Get started in just a few seconds with ongoing support throughout the process. Fast Payments: Enjoy the convenience of cashing out up […]

Full Post at jobs.wane.com

Side Gig: Earn Guaranteed Income Driving with Uber

November 21, 2024 · · Topic: Basic Income · Relevance: bad

1504106993-2

Date Posted:

Recruiter: Uber Location: Arkport, New York Salary: On Application Job Description Earn a guaranteed minimum of $1794 when you complete your first 181 trips with Uber within 30 days! Why Choose Uber? Driving with Uber offers a flexible way to increase your income while fitting around your busy life. Whether you’re looking for a gig, part-time, or full-time role, we’ve got you covered. What You Should Know: Quick Signup: Sign up in just a few minutes and receive assistance along the way. Fast Payments: Access your earnings up to 5 times a […]

Full Post at jobs.kget.com

Part-time Opportunities: Earn Guaranteed Income Driving with Uber

November 21, 2024 · · Topic: Basic Income · Relevance: bad

1504150385-2

Date Posted:

Recruiter: Uber Location: Monroe, Virginia Salary: On Application Job Description Join Uber and earn at least $1726 guaranteed for your first 163 trips! Why Choose Uber? Driving with Uber offers an easy way to supplement your income while enjoying the flexibility that fits your lifestyle—be it part-time, full-time, or seasonal. Key Benefits of Driving with Uber: Quick Signup: Get started effortlessly today with comprehensive support throughout the process. Fast Payments: Access your earnings up to 5 times a day with Uber’s Instant Pay feature. Guaranteed Income: Enjoy guaranteed earnings for your […]

Full Post at jobs.kget.com

Why Guaranteed Income Is the GOAT

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Kandace Creel Falcón, one of Springboard for the Arts’ guaranteed income recipients, designed the billboard "Guaranteed Income is the G.O.A.T." along County Highway 21 in Foxhome, Minnesota. If you were driving by a remote stretch of Minnesota County Highway 210—connecting Wahpeton, North Dakota and Fergus Falls—you would see a massive billboard depicting a painting of three goats. It looks out of place—colorful and vibrant on a desolate stretch of highway mostly used by westbound truckers and locals. On the top left-hand corner of the billboard rests a stark reminder to anyone looking up: "In rural we tend to the […]

Full Post at www.commondreams.org

BIG restrictions worryWalvis Bay residents

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

END POVERTY NOW … The Basic Income Grant (BIG) Coalition yes- terday demonstrated against poverty at various towns, including in the capital Windhoek. The coalition organised nationwide marches to advocate for the implementation of a universal basic income grant for all Namibians under the age of 60. The march was deliberately held on Heroes Day, commemorated annually on 26 August. Walvis Bay residents worry that strict registration requirements might deprive them of receiving money from the government’s basic income grant (BIG).

The Ministry of Gender Equality, Child Welfare and Poverty Eradication is currently busy with registration in various towns […]

Full Post at www.namibian.com.na

Would you rather…�

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Guaranteed income for sure, then I can work on my personal projects without any worries ��✨

kofi_button

1da day ago Would you rather…�1️⃣ Have a guaranteed income for six months 2️⃣ A high-profile collab that could boost your exposure 2Related threads c.i.ryze 1habout an hour ago aaaaaand number 2 <3 (even a buff woman deserves makeup) (this might or might not be my wife’s leather jacket) melanievogltanz 4h4 hours ago I’d love a sketch of Sachmet, Egyptian warrior and health goddess �� I’m currently working on her novel about how she stranded in the […]

Full Post at www.threads.net

Drive with Uber – Earn Guaranteed Income for Your First 192 Trips

November 21, 2024 · · Topic: Basic Income · Relevance: bad

1504068625-2

Date Posted:

Recruiter: Uber Location: Fort Howard, Maryland Salary: On Application Job Description Join Uber and Earn a Minimum of $2529 by Completing Your First 192 Trips! Why Choose Uber? Driving with Uber is a flexible and straightforward way to enhance your income while fitting into your lifestyle, whether you seek part-time or full-time work. Key Benefits: Quick Signup: Get started in just a few moments with our support available throughout the process. Fast Payments: Enjoy the ability to cash out up to 5 times a day with Uber’s Instant Pay feature. Guaranteed […]

Full Post at jobs.kget.com

Part-time Driving Opportunity: Earn Guaranteed Income

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

1503833405-2

Date Posted:

Recruiter: Uber Location: Eaton, Colorado Salary: On Application Job Description Join Uber and earn guaranteed earnings! Complete 140 trips within 30 days to secure at least $1765. Why Choose Uber? Driving with Uber is an excellent way to enhance your income while enjoying the flexibility to set your own hours, whether you’re looking for a part-time gig or a temporary position. Key Details: Quick Sign-up: Start driving today with a simple and fast application process. Support is always available. Fast Payments: Enjoy access to Instant Pay, allowing you to cash out up […]

Full Post at jobs.texomashomepage.com

Federal Minimum Wage Increase 2024, Marking 15 Years Since the Last Raise

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Since its establishment in 1938, the federal minimum wage has served as a baseline for compensating workers across the United States. Intended to provide a minimum standard of living to prevent labour exploitation and poverty, this wage floor has seen periodic adjustments to reflect changes in the economy and cost of living.

However, the most recent update to the federal minimum wage occurred on July 24, 2009, when it was set at $7.25 per hour. This adjustment marked an increase from the previous rate of $6.55 per hour, a change enacted during the first year of former President Barack Obama’s […]

Full Post at yuvagalam.com

Tacoma’s cash assistance pilot program leads to improved quality of life for families

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Tacoma, partnering with United Way of Pierce County, provided 110 recipients with $500 for 13 months. The success of the first program led to another round. More Videos

TACOMA, Wash. — On Tuesday, the results of Tacoma’s Guaranteed Income Pilot Program , known as Growing Resilience in Tacoma (GRIT), were made public. They revealed a profound impact on participating families.

The program, launched in December 2021, provided 110 families with $500 monthly payments for one year, with no strings attached. These families were selected based on their financial circumstances, with many falling into a category referred to as ALICE (Asset […]

Full Post at www.king5.com

OpenAI CEO Received $76,001 In Pay Last Year, Filing Shows

November 21, 2024 · · Topic: Basic Income · Relevance: not sure

Sam Altman is worth at least $2 billion. OpenAI Chief Executive Officer Sam Altman received a modest $76,001 in compensation last year, up slightly from $73,546 in 2022, a newly released tax filing shows.

Altman, who is worth at least $2 billion, has previously said he gets paid "whatever the minimum for health insurance is." He has also repeatedly said he does not own equity in OpenAI. However, the San Francisco-based artificial intelligence startup has discussed giving him a stake as part of a possible shift to becoming a for-profit business, Bloomberg reported.

Altman’s paycheck was included in a filing that […]

Full Post at www.ndtv.com

$725 Monthly Stimulus Check: Know Eligibility Criteria and Payment Timeline

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

FFESP 725 Stimulus Check Announced The rising cost of living has hit low-income families hard, making it difficult to cover basic needs like food, housing, and childcare. To ease this burden, Sacramento has launched the Family First Economic Support Pilot (FFESP) . This initiative offers eligible families $725 monthly for a year, providing consistent financial relief.

Curious about how this program works and who qualifies? Let’s dive into the details.

Table of Contents [ show ] Overview The Family First Economic Support Pilot is a financial aid program targeting low-income families in Sacramento, California. It prioritizes households with young children, especially […]

Full Post at wbza.co.in

Guaranteed income opens for 250 health career students at Community Colleges

November 20, 2024 · · Topic: Basic Income · Relevance: bad

YOU MAY ALSO LIKE

Local News

7 Year-Old "Hung" In School Bathroom By Older Boy – Questioning Zero Tolerance Bullying Laws Debra Blackwell11 hours ago He was accused of an armored car heist. His tattoo helped put him away. Los Angeles Times22 hours ago He Was the Only Black Actor to Appear on TV’s ‘I Love Lucy’: A Look Back at the Life of Sam Daniel Herbie J Pilato15 days ago The Alcoholic Life and Strange Death of Actor William Holden: A Tragic and Sad Look Back Herbie J Pilato6 days ago 4 Cannabis Myths That Need To Die […]

Full Post at www.newsbreak.com

FD Interest Rate: Customers are getting up to 8.75% interest on FD in 10 banks of India

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

FD Interest Rate: Customers are getting up to 8.75% interest on FD in 10 banks of India SBM Bank is paying 8.25% interest to its general customers and up to 8.75% interest to senior citizen customers on FDs ranging from 3 years 2 days to less than 5 years.

FD Interest Rate: If you are planning to invest in Fixed Deposit (FD) then this news is useful for you. By investing in FD, customers get guaranteed income after a certain period. Actually, many private and government banks of the country are offering bumper interest to their customers on […]

Full Post at www.informalnewz.com

Universal basic income will become a necessity as more jobs go AI �

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

ashleydsparkles 22

29

22 dzwiedz24 8h8 hours ago I wonder, who’s making up bullshit without even checking what the supposed AI company does and whether it still exists. Because, funny thing, Q AI was, with the emphasis on "was", a fintech company that shuttered last year.62 brucewmurphy 5h5 hours ago First you’re going to have to wind back the social construct the values people only for the work they do.11 dzwiedz24 5h5 hours ago Yeah, that. Or just start acting like AI-generated content is disposable and of negligible value. For example, a lot of people generated and posted […]

Full Post at www.threads.net

Black Women Can’t Save America From Itself

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

The 2024 U.S. election has left me more shaken than I expected. As the results poured in, I sat frozen with worry, my 14-year-old son Tendekai next to me. Seeing the early exit poll numbers brought a flood of anxiety. When I checked my phone in the middle of the night to see the results confirmed my fears, my thoughts didn’t immediately turn to the impact of the upcoming administration on the guaranteed income work I’ve been growing for nearly a decade in the economic justice movement.

In that moment—and still a few weeks later—I can only think about my […]

Full Post at time.com

NDP statement for National Child Day 2024

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

NDP critic for Families, Children and Social development Leah Gazan (Winnipeg Centre) made the following statement:

“Today, we celebrate National Child Day.

On November 20, 1989, Canada adopted the United Nations Convention on the Rights of the Child, committing to upholding the respect, dignity and full potential of all children. In the same year, Canada also unanimously passed an NDP motion to eliminate child poverty by the year 2000. Thanks to families and advocates, we’ve accomplished so much, but this government still has a long way to go to truly lift families out of poverty.

In 2020, in part […]

Full Post at www.ndp.ca

2 Years On Basic Income: A Personal Story of Transformation

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

Two years ago, I was just like most people: working multiple part-time jobs, barely making ends meet, and constantly worried about whether I’d have enough to cover my rent, bills, and groceries.

Photo by Travis Essinger on Unsplash Two years ago, I was just like most people: working multiple part-time jobs, barely making ends meet, and constantly worried about whether I’d have enough to cover my rent, bills, and groceries. I had dreams, sure, but they felt far out of reach, buried under the weight of survival. Then, something extraordinary happened: I became part of a pilot program for […]

Full Post at vocal.media

Election 2024: Parties commit to continued support for Basic Income for the Arts scheme

November 20, 2024 · · Topic: Basic Income · Relevance: bad

The Basic Income for the Arts pilot scheme has been running since 2022 Via The Journal Of Music : Sinn Féin and the Social Democrats have published their manifestos for the 2024 election. This follows the publication of manifestos from Fianna Fáil and the Green Party last week , and from Fine Gael, Labour, and People Before Profit earlier this week . All manifestos contain sections on the arts.

Sinn Féin and the Social Democrats are each promising to develop a long-term scheme informed by the results of the Basic Income for the Arts pilot, which concludes in August 2025. […]

Full Post at www.rte.ie

HMRC warning over private pensions with more people ‘being caught in net’

November 20, 2024 · · Topic: Basic Income · Relevance: not sure

HMRC warning over private pensions with more people ‘being caught in net’ People with a pension pot risk being dragged into a new Labour Party government and HMRC tax raid. Pension savers risk being "caught in the net" of Rachhel Reeves’s tax reforms, despite Steve Reed insisting only a few hundred farms will be impacted by changes to inheritance tax.

Mike Ambery, Retirement Savings Director at Standard Life, said: "As you don’t need to use the full pension pot when buying an annuity, this approach would allow retirees to provide themselves with a guaranteed income to live on while lessening […]

Full Post at www.birminghammail.co.uk